Cards In This Set

| Front | Back |

|

1 Introduction

Why is pricing important?

|

1 Introduction

- It makes a pivotal contribution to profit maximisation – the overriding aim of most businesses

- Businesses make profits by selling goods and services at a price higher than their cost

- The amount that they are able to sell will often be determined by the price charged for the goods and services

|

|

2 Different types of market structures

1) What is a perfectly competitive market?

2) Characteristics

|

2 Different types of market structures

1) In a perfectly competitive market, every buyer or seller is a 'price taker', and no participant influences the price of the product it buys or sells.

2)

- Zero Entry/Exit Barriers – It is relatively easy to enter or exit as a business in a perfectly competitive market.

- Perfect Information - Prices and quality of products are assumed to be known to all consumers and producers.

- Companies aim to maximise profits - Firms aim to sell where marginal costs meet marginal revenue, where they generate the most profit.

- Homogeneous Products – The characteristics of any given market good or service do not vary across suppliers.

|

|

2 Different types of market structures

1) What is Imperfect competition

2) What forms does it take?

|

2 Different types of market structures

1) Imperfect competition refers to the market structure that does not meet the conditions of perfect competition.

2)

- Monopoly, in which there is only one seller of a good. The seller dominates many buyers and can use its market power to set a profit-maximising price. Microsoft is usually considered a monopoly.

- Oligopoly, in which a few companies dominate the market and are inter-dependent : firms must take into account likely reactions of their rivals to any change in price, output or forms of non-price competition. For example, in the UK, four companies (Tesco, Asda, Sainsbury's and Morrisons) share 74.4% of the grocery market.

- Monopolistic competition, in which products are similar, but not identical. There are many producers ('price setters') and many consumers in a given market, but no business has total control over the market price.

|

|

3 Three broad approaches to pricing

What are the three broad approaches to pricing?

|

3 Three broad approaches to pricing

1) Demand-based approaches

2) Cost-based approaches

3) Marketing-based approaches

|

|

4 Demand-based approaches (The Economists' Viewpoint)

What is the relationship between the selling price of a product/service and the demand?

|

4 Demand-based approaches (The Economists' Viewpoint)

Inverse, linear relationship:

|

|

4 Demand-based approaches (The Economists' Viewpoint)

What are the two methods of solution to problems investigating the relationship between price and demand?

|

4 Demand-based approaches (The Economists' Viewpoint)

The tabular approach and the algebraic approach.

|

|

5 The algebraic approach

As per Economic theory, monopolist maximises profit when?

|

5 The algebraic approach

Marginal Cost = Marginal Revenue.

|

|

5 The algebraic approach

1) What is marginal cost?

2) What is marginal revenue?

|

5 The algebraic approach

1) Marginal Cost is the cost from making one more unit. It is usually just the variable cost

2) Marginal Revenue is the additional revenue from selling one extra unit,

|

|

6 Procedure for establishing the optimum price of a product

What are the general rules that can be applied to most questions involving algebra and pricing.

|

6 Procedure for establishing the optimum price of a product

1) Establish the linear relationship between price (P) and quantity demanded (Q). The equation will take the form:

P = a + bQ where 'a' is the intercept and 'b' is the gradient of the line. As the price of a product increases, the quantity demanded will decrease. The equation of a straight line P= a + bQ can be used to show the demand for a product at a given price

2) Double the gradient to find the marginal revenue:

MR = a − 2bQ

3) Establish the marginal cost MC. This will simply be the variable cost per unit

4) To maximise profit, equate MC and MR and solve to find Q

5) Substitute this value of Q into the price equation to find the optimum price

6) It may be necessary to calculate the maximum profit.

|

|

6 Procedure for establishing the optimum price of a product

1) What does the price elasticity of demand measures?

2) What is the equation?

|

6 Procedure for establishing the optimum price of a product 1) The price elasticity of demand measures the change in demand as a result of a change in its price 2) The negative sign should be ignored in the PED calculation |

|

6 Procedure for establishing the optimum price of a product

If the % change in demand > the % change in price, then price elasticity > 1

|

6 Procedure for establishing the optimum price of a product

- Demand is ‘elastic’, i.e. very responsive to changes in price.

- Total revenue increases when price is reduced

Total revenue decreases when price is increased

- Therefore, price increases are not recommended but price cuts are recommended

|

|

6 Procedure for establishing the optimum price of a product

If the % change in demand < the % change in price, then price elasticity < 1

|

6 Procedure for establishing the optimum price of a product

- Demand is ‘inelastic’, i.e. not very responsive to changes in price.

- Total revenue decreases when price is reduced.

Total revenue increases when price is increased

- Therefore, price increases are recommended but price cuts are not recommended

|

|

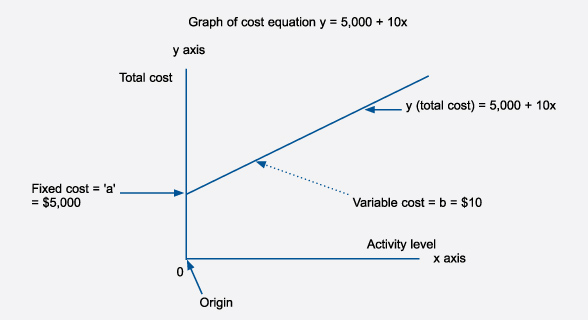

7 Equation for the total cost function

What is the cost function equation?

What do the letter represent?

|

7 Equation for the total cost function y = ax + b y = total cost a = variable cost/unit x = units b = fixed costs |

|

Cost-based pricing: the accountant’s approach

What is cost plus pricing?

|

Cost-based pricing: the accountant’s approach

'Cost plus' pricing is a much favoured traditional approach to establishing the selling price by calculating the unit cost adding a mark-up or margin to provide profit.

|

|

Cost-based pricing: the accountant’s approach

Whay type of business is cost-plus pricing is more suited to?

|

Cost-based pricing: the accountant’s approach

Business that sell the product in large volumes operate in markets dominated by price.

|